Why Debt is King in Wall Street: A Deep Dive into Leveraged Buyout Mechanics

by Divya

3/19/20264 min read

In the world of elite corporate finance, few strategies command as much capital—or controversy—as the Leveraged Buyout (LBO). Executed by powerhouse Private Equity (PE) firms like Blackstone, Carlyle, or KKR, an LBO is the financial equivalent of purchasing a corporate empire using a massive mortgage.

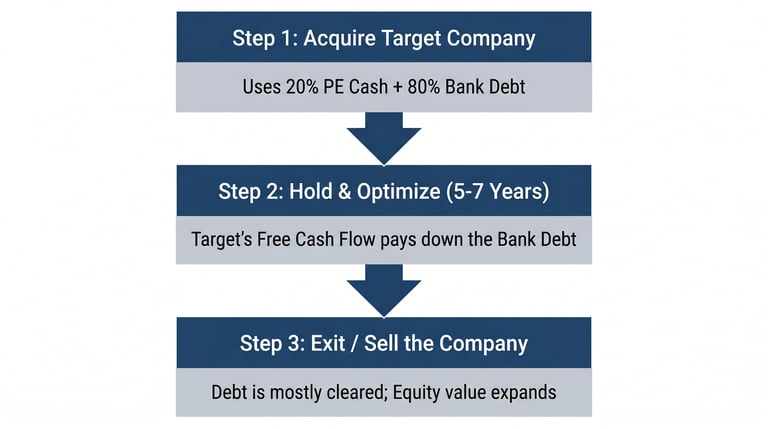

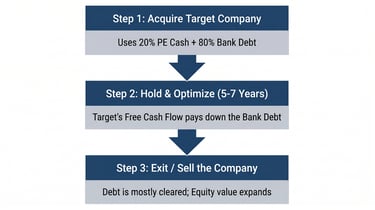

An LBO involves acquiring a company using a small amount of equity (cash) and a massive amount of borrowed money (debt). The private equity firm then uses the acquired company’s own cash flows to pay off that debt over time, eventually selling the business for an exponential return.

This case study breaks down the mechanics of the LBO model, explores the financial engineering frameworks taught in top-tier MBA programs, and illustrates how debt functions as an aggressive amplifier of investment returns.

1. The Core Framework: The Power of Financial Leverage

To understand why private equity firms rely so heavily on debt, you must look at how leverage fundamentally changes the math of a corporate acquisition.

Think of it like buying a house. If you buy a $1,000,000 property entirely with cash and sell it later for $1,200,000, your return on equity is a modest 20%. But if you buy that same house putting down only $100,000 of your own cash and borrowing the remaining $900,000, that same $200,000 price increase yields a staggering 200% return on your equity.

In an LBO, a private equity firm applies this exact mathematical principle to entire corporations, typically structuring a deal with 60% to 80% debt and only 20% to 40% equity.

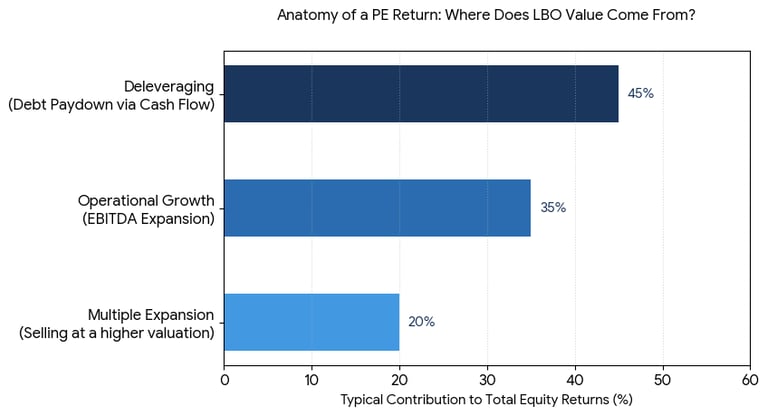

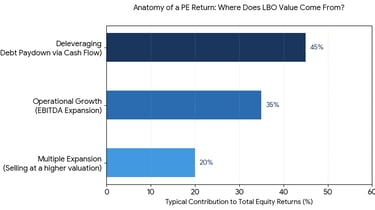

2. Visualizing Value Creation: The Three LBO Return Drivers

An LBO creates massive financial returns through three distinct levers. While operationally improving a business matters, the mathematical core of the playbook relies heavily on the structural paydown of leverage.

Deleveraging (Debt Paydown): As shown in the graph, this is often the most important driver. Even if the company's total enterprise value stays exactly the same, reducing the debt balance automatically transfers value over to the equity holders.

Operational Growth (EBITDA Expansion): Private equity firms cut unnecessary corporate overhead, streamline operations, and invest in high-margin product lines to expand earnings before interest, taxes, depreciation, and amortization.

Multiple Expansion: Buying a company at a lower valuation multiple (e.g., 8x EBITDA) and selling it years later at a premium multiple (e.g., 10x EBITDA) by transforming it into a faster-growing, lower-risk enterprise.

3. The Target Profile: What Makes a Perfect LBO Candidate?

Private equity firms evaluate thousands of corporations every year, but very few companies possess the specific financial traits required to safely carry such massive amounts of leverage. A perfect LBO target must fit a highly selective profile:

Stable and Predictable Free Cash Flows: This is the most crucial requirement. Because debt payments are mandatory, a company with volatile or cyclical earnings faces an immediate risk of default.

Low Existing Debt Load: The target must have a relatively clean balance sheet so the PE firm can layer on new, senior-secured acquisition debt.

Strong, Defensible Market Position: High barriers to entry, recurring revenue streams, and sticky customer bases protect the cash flows needed to clear the debt schedule over time.

Non-Core or Underutilized Assets: Businesses with unoptimized real estate, bloated administrative layers, or underperforming divisions provide immediate opportunities to extract quick cash infusions to pay down principal debt early.

4. Risks and Guardrails: The Dark Side of Financial Engineering

While LBOs can generate extraordinary Internal Rates of Return (IRR) for institutional investors, the model carries severe structural risks.

When you load an enterprise with extreme debt, you dramatically lower its margin for error. If an unexpected macroeconomic downturn hits, or a new competitor disrupts the market, a leveraged company can rapidly find its operating income wiped out by fixed interest obligations.

Historically, aggressive LBO structures have driven iconic retail brands (such as Toys "R" Us and Caesars Entertainment) into bankruptcy court when debt service outpaced operational cash generation. To combat this, modern corporate finance mandates strict structural guardrails, including mandatory interest rate swaps to hedge against rising rates, and covenant-lite debt facilities to give companies operational breathing room during sudden economic shocks.

Key Takeaways for Corporate Managers

Optimize Capital Structure: Equity capital is expensive; debt capital is cheaper due to tax-deductible interest. Finding the optimal mix of both can lower your Weighted Average Cost of Capital (WACC) and boost equity returns.

Focus on Cash Conversion: Net income is a great accounting metric, but debt is serviced exclusively out of free cash flow. Prioritize working capital management to keep cash moving quickly through the balance sheet.

Efficiency Drives Value: Every dollar of operational waste eliminated doesn't just improve your margin—in a leveraged environment, that dollar directly unlocks capital to reduce debt or fund strategic growth.

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.