The Illusion of Control: What Enron Teaches Us About Risk Assurance Failures

by Divya

3/18/20263 min read

In the corporate hierarchy, the Risk Assurance and Internal Audit functions serve a singular purpose: to protect an organization from its own blind spots. They act as independent internal safeguards, evaluating risk management, operational integrity, and executive compliance.

But in 2001, when Enron Corporation imploded under a $74 billion mountain of hidden debt, it exposed the biggest systemic risk assurance breakdown in business history.

Enron didn't fail because it lacked a risk management department. In fact, it had one of the most sophisticated, highly praised risk infrastructure frameworks on paper. It collapsed because its corporate structure actively dismantled, compromised, and bypassed every single line of defense.

This case study analyzes Enron through the lenses of modern internal controls and corporate risk frameworks to show how a culture of unchecked compliance can result in complete corporate disaster.

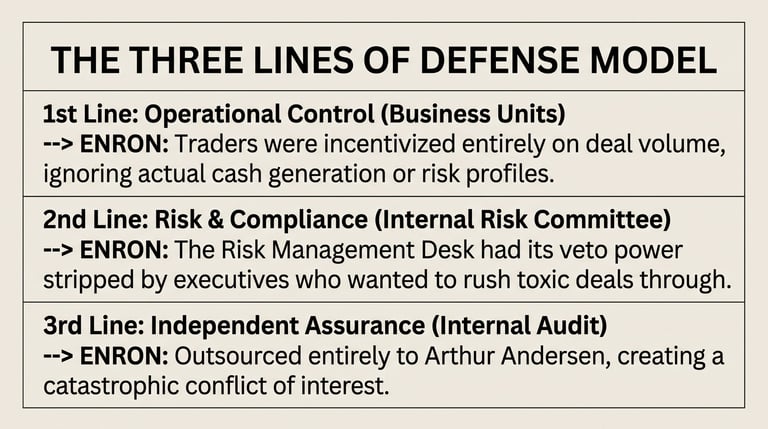

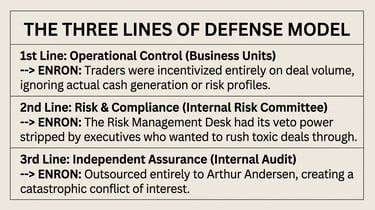

Modern risk assurance relies on the Three Lines of Defense framework to ensure proper governance and accountability. Enron's downfall was a complete, concurrent structural failure across all three levels:

When senior executives actively silence the second line and compromise the independence of the third, the entire assurance framework transforms from a defensive shield into an optical illusion for investors.

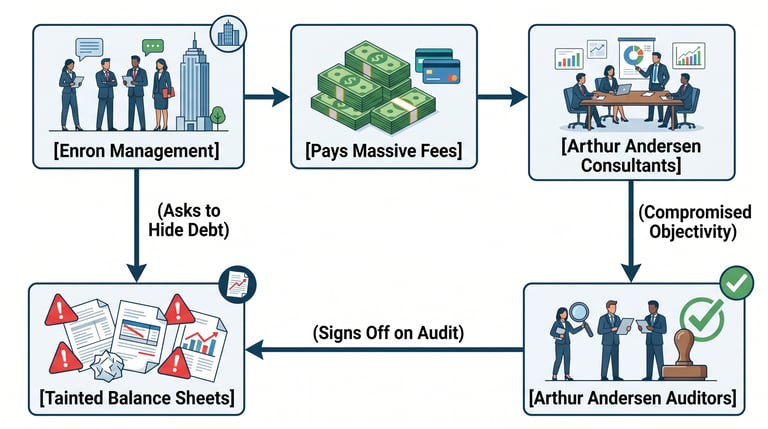

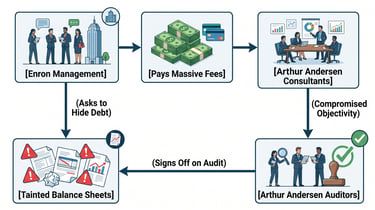

2. Structural Failure: The Danger of Co-Sourcing Audit Functions

The single most glaring breakdown in Enron's risk assurance strategy was its relationship with its auditor, Arthur Andersen.

Instead of maintaining a clear, distinct boundary between external validation and internal operations, Enron pioneered an aggressive co-sourcing model. They hired Arthur Andersen to perform both their independent external audit and run their internal audit function.

This arrangement obliterated any chance of objective risk assurance. Because Arthur Andersen was making millions of dollars providing lucrative business consulting services to Enron, the firm’s auditing division was heavily disincentivized from raising red flags about Enron's complex off-balance-sheet shell companies.

3. The Ultimate Governance Failure: Waiving the Code of Ethics

Risk assurance can only function if the tone at the top respects institutional guardrails. At Enron, the Board of Directors actively compromised internal governance by taking unprecedented steps to clear paths for high-risk behavior.

To keep massive liabilities hidden, Chief Financial Officer Andrew Fastow established private partnerships known as Special Purpose Entities (SPEs) to buy up Enron’s toxic, underperforming assets. Because Fastow stood to gain millions personally from these shell networks, Enron's internal code of conduct explicitly forbade it.

In a catastrophic governance failure, the Enron Board of Directors voted multiple times to waive the company's own Code of Ethics. This choice permitted Fastow to manage the conflict of interest, neutralizing the internal controls that were meant to halt self-dealing and high-stakes financial risk.

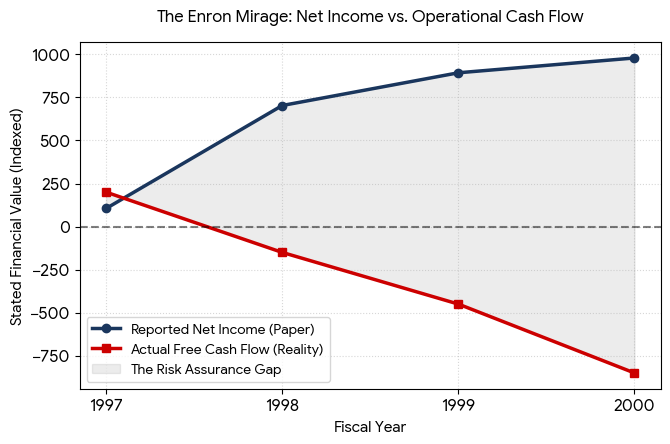

4. Visualizing the Disconnect: Reported Profits vs. Actual Cash

The clearest red flag of Enron's failed internal risk assurance loop was the widening chasm between paper bookkeeping and cold, hard liquidity. While accounting frameworks can be manipulated, cash balances are absolute facts.

Because the risk assurance function was systematically neutralized, no internal body forced a reconciliation of this divergence. This gave executives free rein to burn cash until the entire structural framework collapsed.

Key Takeaways for Risk Professionals

Assurance Requires Absolute Independence: Internal Audit must report directly to the independent audit committee, completely separated from corporate management or executive bonus structures.

Beware of Compliance Theater: Having complex risk manuals, heat maps, and committees means nothing if executives retain the unchecked power to bypass controls at will.

Investigate Red Flags Aggressively: The primary duty of risk assurance is to follow unexplained financial anomalies, no matter how complex or protective senior leadership tries to be.

Explore More Business Articles

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.