The November Inflation Report Is a Massive Relief, But We Should Still Be Skeptical.

by Divya Kolmi

12/31/20253 min read

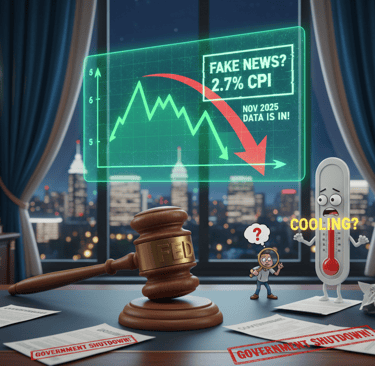

The U.S. Bureau of Labor Statistics (BLS) finally dropped its much-delayed November inflation report today, and if you listen to Wall Street, it's nothing short of a miracle. Inflation is cooling, and it’s doing so faster than anyone expected. On the surface, the numbers – a 2.7% annualized CPI and a 2.6% Core CPI – are music to the ears of investors and, more importantly, to a Federal Reserve that has been battling persistent price hikes for what feels like an eternity.

But I have to admit, there's a part of me that's raising an eyebrow. A big one.

A Data Report Unlike Any Other

Let's not forget the elephant in the room: the government shutdown. From October 1st to November 12th, the BLS was effectively sidelined. This wasn't just a slight delay; it meant they couldn't collect the full slate of data they normally would for October, and had to get "creative" with November's numbers, using "nonsurvey data sources" and imputation methods.

While the BLS assures us the data is robust, it begs the question: how precise can these numbers truly be when a significant chunk of raw data was simply unavailable?

Economists are already sounding notes of caution, and I think they're right to do so. Calling this a "permanent trend" based on data collected under such unusual circumstances might be premature. My concern is that we're seeing something of a statistical mirage – a picture that looks fantastic, but might be slightly distorted by the very unique circumstances of its creation.

The "Shelter" Silver Lining – But Is it Enough?

The biggest win, undoubtedly, comes from the shelter sector. After being the thorn in the Fed's side for so long, shelter costs rising at "just" 3% annually is genuinely encouraging. This is the sticky inflation the Fed has been desperate to see ease, and it’s a crucial component of overall CPI. If this trend holds, it's a huge step towards the Fed's 2% target.

However, even here, I wonder if the methods used to estimate these costs during the shutdown period might have played a role. Are we seeing the true, organic cooling of the housing market, or is there an element of statistical smoothing influencing this number?

The "Fed Put" is Back – A Risky Proposition?

The market's reaction was swift and decisive: Treasury yields tumbled, and S&P 500 futures jumped. The narrative is clear: a "tame CPI" means the Fed will pivot, shifting focus from inflation to protecting the labor market. The "Fed Put" – the belief that the Fed will intervene with rate cuts if the economy falters - is back with a vengeance, with a March 2026 rate cut now looking more likely.

While I appreciate the market's optimism, I can't shake the feeling that we might be getting ahead of ourselves. Relying heavily on potentially "noisy" data to justify such a significant policy shift could be risky. What if the January 2026 report, collected under normal conditions, paints a different picture? What if the underlying inflationary pressures are still bubbling, just obscured by the shutdown's statistical fog?

My Conclusion

Don't get me wrong, I want to believe inflation is truly cooling. It's good for everyone. But given the unprecedented nature of this data release, I am exercising extreme caution.

For me, the November 2025 CPI report is less of a definitive victory and more of a "wait and see" situation. The January 2026 report, with its cleaner data collection, will be the real litmus test. Only then will we truly know if this cool-down is a genuine trend or just a fortunate side effect of a very "messy" November.

Explore More Business Articles

Contact

Questions? Reach out anytime.

© 2025 BizSphere. All rights reserved.